TranceAddict Forums (www.tranceaddict.com/forums)

- Political Discussion / Debate

-- Stimulus package full of pork?

Pages (4): « 1 2 [3] 4 »

Ok well PK was a somewhat correct in that your initial response didn't really answer my questions, but your subsequent response to his post gives me some understanding of what your position is.

| quote: |

| Originally posted by Capitalizt I said that I preferred fiscal stimulus that focuses on tax relief over expanded welfare programs. |

| quote: |

I thought I explained my opposition to almost every aspect of the bailout, including everything the fed has done in the past 12 months. All of the programs oc mentioned have done essentially the same thing (drastically increase the money supply). This is only postponing the inevitable. Things need to correct, and the only alternative is temporary prosperity bought by trillions in additional debt and the destruction of the dollar. Let the market correct. It will be ugly, but it is the lesser of two evils. |

| quote: |

| Originally posted by jerZ07002 the common misconception among people is that high capital gains taxes prevents investment. This idea is ridiculous because people would rather have their money earn 70% (assuming a 30% tax rate) of their gain, than 0% of no gain. The impediment caused by a high capital gains rate is that sometimes people with gains that would be taxed at the capital gains rate may not move their investments because they don't want to pay taxes on that gain. However, there is only a taxing preference if the capital asset is held for a long term (> 1 year), which means assets with rate preferences can't be flipped, and must be held for a period over which that person will likely recapture the lost taxes by a higher return (which is the entire purpose for making a new investment). Admittedly, there is a small impediment to the movement of capital by higher rates, however, it also means new investments will be more highly scrutinizes, which means the money likely will be invested in the most economically efficient manner. Example: (1) asset currently appreciates 5% annually, and you have a 100 gain recognized on the sale of the asset (2) 15% tax on gain is $15, and at 30% is $30. (3) new asset appreciates 10% annually. It would only take 3 years to recover that difference with the excess return on appreciation (the extra 5% return on asset). The entire point of preferential rates is that the asset is held for a long period (thus the incentive are actually in line with congressional purpose), and it furthers the most efficient use of capital. |

| quote: |

| Originally posted by occrider With respect to fiscal stimulus, I think I would disagree with you in terms of concentration of fiscal stimulus, however it seems that you accept that all forms of fiscal stimulus: infrastructure spending, social services spending, and tax cuts are all necessary. I think I might disagree with you with respect to the understanding that I think that social services spending (unemployment, welfare, etc.) are absolutely required since they are universally regarded by economists as automatic stabilizers in the business cycle (they tend to smooth erratic swings in consumer spending and thus minimize recessionary troughs). |

| quote: |

| Originally posted by occrider The second area I might disagree with you is that I think that tax cuts, whilst having a faster velocity to impact (a reduction in payroll taxes can happen in a few weeks or months) are less effective than spending increases particularly in recessions such as this. The reason why I say this is because with every dollar spent in feral spending, you are guaranteed a dollar increase in GDP, with every dollar spent in federal spending, tax cuts do not follow that same parameter because consumers have the option to SAVE money. As such a dollar of fiscal stimulus in tax cuts may well result in less than a dollar in GDP growth. The problem with the tax cuts of last year was that it was estimated that 2/3rds to 4/5ths were not spent at all. Money not spent in fiscal stimulus is money wasted. If one were to look at the fiscal stimulus multiplier, the most effective forms of fiscal stimulus are social welfare programs (a no brainer because people will always spend money rather than starve) and infrastructure projects. What is particularly alluring about infrastructure projects is that the ALSO contribute towards long term growth in GDP. Btw, in a studies done by moody's you can see their forecasted multiplier impacts for fiscal stimulus components: http://www.economy.com/mark-zandi/d...ess_7_24_08.pdf |

| quote: |

| Originally posted by occrider I think I might disagree with you with respect to the understanding that I think that social services spending (unemployment, welfare, etc.) are absolutely required since they are universally regarded by economists as automatic stabilizers in the business cycle |

I've realized the errors of going to a pure gold standard and don't agree completely with the articles below, but I do think if we had a fed/treasury intent on reducing intervention and maintaining a stable currency, the economy would tend to balance much closer towards equilibrium over time, and many of the painful "busts" could be eliminated.

I've realized the errors of going to a pure gold standard and don't agree completely with the articles below, but I do think if we had a fed/treasury intent on reducing intervention and maintaining a stable currency, the economy would tend to balance much closer towards equilibrium over time, and many of the painful "busts" could be eliminated. | quote: |

The second area I might disagree with you is that I think that tax cuts, whilst having a faster velocity to impact (a reduction in payroll taxes can happen in a few weeks or months) are less effective than spending increases particularly in recessions such as this. The reason why I say this is because with every dollar spent in feral spending, you are guaranteed a dollar increase in GDP, with every dollar spent in federal spending, tax cuts do not follow that same parameter because consumers have the option to SAVE money. As such a dollar of fiscal stimulus in tax cuts may well result in less than a dollar in GDP growth. The problem with the tax cuts of last year was that it was estimated that 2/3rds to 4/5ths were not spent at all. Money not spent in fiscal stimulus is money wasted. |

The Republican Party is seriously disconnected from reality right now... they seem to be openly prescribing to the "I hope we fail" mindset of Rush - just so they can play partisan politics and blame the impending disaster on Obama.

| quote: |

| Elana Schor has a post this morning showing the four Senate Republicans who appear to be in play for President Obama on the Stimulus Bill, based on their vote last night on Sen. DeMint's alternative Stimulus Bill. But there's something else last night's vote tells us. There were 36 out of 41 Republican senators who voted to scrap all spending in the Stimulus Bill. All of it. This approaches flat earth territory in terms of where the economy is right now and what conventional macroeconomics suggests about how to combat the problem. |

Another danger that isn't oft reported:

| quote: |

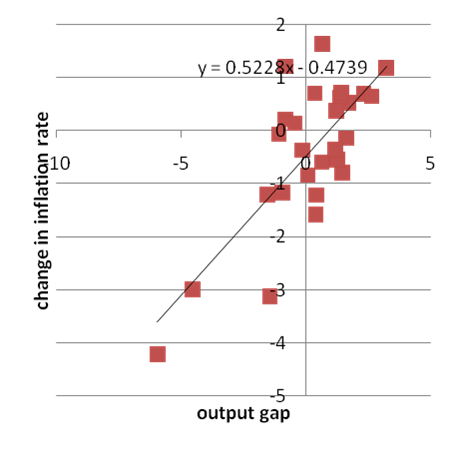

About that deflation risk Look out below There has been a distinct change in tone from the Obama team today, as they seem to have become suddenly aware that there�s a real risk that the stimulus plan will either fail to pass, or be emasculated to the point that it doesn�t come close to doing the job. Obama himself has warned of catastrophe if we fail to act, and � finally!� denounced the tax-cut philosophy. Meanwhile, Larry Summers has finally made the point I�ve been pushing for a while � that we�re at major risk of falling into a deflationary trap. I thought it might be useful to present a bit of evidence behind that concern. The figure above plots an estimate of the output gap � the difference between actual and potential GDP, as a percentage of potential � and the change in the inflation rate. Both series are taken from the IMF WEO database, for convenience, and use data from 1980-2007. It�s not a perfect fit � this is economics, not physics, and anyway stuff besides the output gap bounces inflation around from year to year. But still, there�s a clear correlation, driven largely but not entirely by the deep slump and disinflation of the early 1980s, and an implied slope of about 0.5 � that is, every percentage point by which real GDP fall short of potential tends to reduce the inflation rate by about half a point over the course of the year. And right now the CBO is saying that in the absence of a policy action the average output gap will average 6.8 percent over the next two years. Do the math: if anything like the historical relationship between output and inflation holds, we�re looking at major deflation. OK, maybe that relationship won�t hold � getting to actual deflation may take a deeper slump than merely reducing the inflation rate. And maybe a regression driven in part by 80s data isn�t a good guide to current events. But deflation is a huge risk � and getting out of a deflationary trap is very, very hard. We truly are flirting with disaster. |

| quote: |

| Originally posted by Lebezniatnikov The Republican Party is seriously disconnected from reality right now... they seem to be openly prescribing to the "I hope we fail" mindset of Rush - just so they can play partisan politics and blame the impending disaster on Obama. http://www.talkingpointsmemo.com/ar...rthal_party.php Getting really sickening to watch this unfold. |

| quote: |

| You see, this isn�t a brainstorming session � it�s a collision of fundamentally incompatible world views. If one thing is clear from the stimulus debate, it�s that the two parties have utterly different economic doctrines. Democrats believe in something more or less like standard textbook macroeconomics; Republicans believe in a doctrine under which tax cuts are the universal elixir, and government spending is almost always bad. Obama may be able to get a few Republican Senators to go along with his plan; or he can get a lot of Republican votes by, in effect, becoming a Republican. There is no middle ground. |

Thats why I've said since the beggining of this whole ordeal that Obama needs to stop giving a fuck about what they want.

| quote: |

| Originally posted by Clovis Thats why I've said since the beggining of this whole ordeal that Obama needs to stop giving a fuck about what they want. |

| quote: |

| Originally posted by Capitalizt I've realized the errors of going to a pure gold standard |

| quote: |

| Originally posted by pkcRAISTLIN well, its good to see you're making progress! |

| quote: |

"...A self-respecting central bank refrained from printing an excess of currency as well as from monetizing its government's debts. Neither did it buy, to excess, assets denominated in currencies not its own (compare today's stockpiling of Treasurys by Asian central banks). The everyday business of a central bank was to exchange its currency for gold and gold for its currency at the stipulated, fixed rate. It was monetary minimalism. In this long departed Age of Taboos--roughly 1815-1914--currencies were stable, interest rates low and business cycles volatile. Prices rose in wartime and fell in peacetime, and they weren't much higher at the end of the 100 years than they were at the start. Reciprocity was a hallmark of that system but not of any successor system, most especially the one in place in 2009. Deficit countries remitted money; surplus countries received it. But the remittance and the acceptance also corrected the preceding imbalance. The following description of the process of adjustment, dating from 1932 (thank you Bank for International Settlements) not only explains how the classical gold standard worked, but also why other standards, or non-standards, have not worked. "If for reasons connected with the exchange rate, country A is compelled to surrender gold to country B, it not only equalizes an unfavorable balance of payments by the export of gold, but also--and this is far more important--influences the component parts of that balance. Gold exports normally entail a curtailment of the domestic volume of credit, higher interest rates, a tendency for prices to drop, increased exports and restricted imports, that is, the elimination of those factors which normally led to the efflux of gold. Inversely, country B does not merely collect a favorable balance of payments in gold, since a gold inflow normally entails credit expansion, lower interest rates, a tendency for prices to rise, reduced exports and augmented imports. Gold movements thus have a reciprocal effect: they not only tend to cause a restriction of credit with all the attendant consequences in the country surrendering gold, but also tend to produce a corresponding credit expansion in the country receiving gold. Country B may be said to meet country A halfway in adjusting the balance of payments." A moment of silence, please, for this system, nobody's creation but everyone's helpmeet. Nevertheless, it ended. Conscripted into the Great War, central banks printed money without reference to their gold reserves, and they monetized their governments' enormous borrowings. Four years after the Armistice, in 1922, the taboo-constrained prewar monetary system got a modern makeover. In place of the delicate, remarkably self-regulating machinery of the true-blue gold standard, the monetary engineers partly substituted the discretion of central bankers. It was called the gold-exchange standard, and we linger over its memory because it has never really gone away. At a glance, the gold-exchange standard was not so radically different from its predecessor. Yet, though the forms of the prewar system remained in place, the substance was gone. Yes, currencies were still defined as a weight of gold and were exchangeable into gold, or into other currencies that themselves were anchored by gold. But the coins and ingots were immobilized. No longer did spontaneous movements of gold and credit regulate the flow of funds among gold-standard nations. More and more, the central bankers took it upon themselves to steer money hither and yon. Why bother at all with gold? It was a question that apparently never came up as politicians and economists tried to put the international financial order back together again. American populists for decades had demanded fiat money, i.e., greenbacks, in place of the scarcer, gold-backed kind. In Europe, however, and in the United States, too, investors of the early 20th century could not imagine a gold-less, taboo-free system. Still, they raised no recorded rumpus over the shucking off of one of the key strictures of the classical gold standard. Under the newfangled gold-exchange standard, central banks began to accumulate heavy volumes of foreign exchange, or securities denominated in foreign exchange, rather than gold. What this practically meant was that a country suffering a monetary drain did not have to tighten credit in order to restore itself to competitive trim. Or, a clarification: It meant that a privileged country suffering an external monetary drain did not have to tighten credit. In the 1920s, Britain was that privileged country. It was still the financial center of the world, though no longer its top industrial power. When money left Britain for greener, more remunerative pastures--France, for instance--the Bank of France did not now automatically convert the pounds it received into bullion, which would have shrunk Britain's monetary base. Rather, the French invested the funds in British securities. It was as if the money never left the City of London. Here was the signal monetary innovation of the 1920s. A deficit country could lose gold, yet not lose it, even though the creditor did actually gain it. The same pound note could support credit growth at home and abroad. It was the dawn of "deficits without tears." One war later, the United States assumed the mantle of the privileged nation, printer of the world's reserve currency, a role it has yet to relinquish. For the past 25 years, America's deficits on current account have piled up, yet--behold!--the dollars have returned to the 50 states in the shape of creditor-nation investments in Treasurys and mortgage-backed securities. We lose dollars, but we really don't lose them. Yet, though we really don't lose them, China really does gain them. It's on this double-duty dollar base that the world has built its tower of leverage. If the immediate cause of today's crack-up is excessive lending and borrowing, the remote cause is the falling away of taboos. It is worth pausing to reflect just how many have tumbled in the past 80 or 90 years. Let us imagine the prewar gold standard as a blue suit, white shirt and necktie. Then the gold-exchange standard would be slacks, a blazer and open-neck shirt--it did retain some starch and structure. Next came the post-WWII Bretton Woods system (of which more in a moment). Call it business casual without the blazer and no socks, either. The post-Bretton Woods arrangements, starting in 1971 and still in place, would be jeans, a T-shirt and flip-flops..." |

The debate continues in the Senate, though it looks like Collins and Nelson will continue their grandstanding in order to "find a solution" - if anybody has figured out the logic behind their proposed cuts, please clue me in.

In the meantime, Republicans are arming up to defeat the bill. And Robert Reich is calling them out for it.

| quote: |

| Senate Republicans and the Stimulus: Playing Politics When the Economy Burns February 5, 2009, 11:54AM Tomorrow's job report is likely to be awful. January's job losses could easily top half a million. We're deep into the most vicious of economic cycles: Consumers are slashing their spending because they're perilously in debt and worried about keeping their jobs. But as a result, businesses are facing shrinking sales of goods and services, so they're slashing payrolls, which of course makes consumers even more anxious and further reduces their spending power. Meanwhile, businesses are cutting way back on new investments in equipment, which hurts upstream suppliers, who are now slashing their payrolls. And so it goes, downward. The gap between what the economy could produce if it were running near full capacity and what it's now producing continues to widen. The shortfall is projected to be over a trillion dollars this year. How do we get out of this downward plunge? Regardless of your ideological stripe, you've got to see that when consumers and businesses stop spending and investing, there's only entity left to step into the breach. It's government. Major increases in government spending are necessary, and the spending must be on a very large scale. In the last several weeks the President has put forward the outlines of a stimulus plan, and has left it to the House and Senate to fill in the details. A tiny portion of the details that made it into the House version should be stripped away because they seem like old-fashioned pork. But most spending in the bill is absolutely appropriate. My worry is there's not nearly enough of spending to fill the shortfall in overall demand. Yet at this very moment, Senate Republicans are seeking to strip the President's stimulus package of many of its spending provisions and substitute tax cuts. Part of this is pure pander: They know tax cuts are more popular with the public than government spending, even though spending is a far more effective way to stimulate the economy (more on this in a moment). Another part is pure partisan politics: Republicans are emboldened by Obama's willingness to court Republicans (taking three Republicans into his cabinet, bringing Republican leaders into the White House for consultations, putting all those business tax cuts into the stimulus bill in order to gain Republican favor) without getting anything at all back from the GOP. House Republicans snubbed the bill entirely. So, Senate Republicans say to themselves, what's to lose? Plenty. Millions more jobs and a full-fledged Depression, for example. Can we get real for a moment? Take a look at this chart, which comes from calculations by Mark Zandy and his colleagues at economy.com. You see that each dollar of spending has much more impact than each dollar of tax cut.  There are three reasons for this. First, most people who receive a tax cut don't spend all of it. They use part of it to pay down their debts or they save it. Most of us did one or the other last spring with that tax rebate. From the standpoint of any particular individual, paying down debts or saving may be smart behavior -- even commendable. But what's intelligent for an individual does not necessarily translate into what's good for the economy as a whole. The only way to get businesses to create or preserve jobs is through additional spending. And unlike tax cuts used to pay down personal debt or add to savings, every dollar of government spending flows directly into the economy and adds to overall demand. Second, even that portion of a tax cut we might actually spend doesn't necessarily go into the American economy. It goes all over the world. I have nothing against creating or preserving the jobs of Asians who assemble those flat-panel TVs you see at the mall, for example, but right now we're trying to create or preserve jobs here in America. Sure, the retail workers at the mall who sell the flat-panel TV's might benefit, but remember we're talking about how to get the biggest bang for every dollar. When government spends to repair a highway or build a school or help pay for medical services, the money and the jobs stay here in America. Finally, those who say cutting taxes on businesses is the best way to create or preserve jobs forget about the demand side. Even with a tax cut, businesses won't hire workers unless there are customers to buy what those workers produce. A government stimulus that creates jobs is a necessary precondition. This isn't a matter of more or less government, however much Republicans and conservatives would like to wedge it in that old ideological box. The issue is how to revive the economy. When consumers and businesses can't or won't spend enough to keep the economy going, government has to be the spender of last resort. Period. |

sometimes we got to laugh

| quote: |

| February 7, 2009, 5:36 pm What the centrists have wrought I�m still working on the numbers, but I�ve gotten a fair number of requests for comment on the Senate version of the stimulus. The short answer: to appease the centrists, a plan that was already too small and too focused on ineffective tax cuts has been made significantly smaller, and even more focused on tax cuts. According to the CBO�s estimates, we�re facing an output shortfall of almost 14% of GDP over the next two years, or around $2 trillion. Others, such as Goldman Sachs, are even more pessimistic. So the original $800 billion plan was too small, especially because a substantial share consisted of tax cuts that probably would have added little to demand. The plan should have been at least 50% larger. Now the centrists have shaved off $86 billion in spending � much of it among the most effective and most needed parts of the plan. In particular, aid to state governments, which are in desperate straits, is both fast � because it prevents spending cuts rather than having to start up new projects � and effective, because it would in fact be spent; plus state and local governments are cutting back on essentials, so the social value of this spending would be high. But in the name of mighty centrism, $40 billion of that aid has been cut out. My first cut says that the changes to the Senate bill will ensure that we have at least 600,000 fewer Americans employed over the next two years. The real question now is whether Obama will be able to come back for more once it�s clear that the plan is way inadequate. My guess is no. This is really, really bad. |

| quote: |

| Originally posted by Shakka Capitalizt--you ever read Jim Grant? Brilliant and a gold bug of sorts. The current issue was particularly good, discussing going from a true classical gold standard to a "gold-exchange" standard, to the fast & loose fiat currency we have now. |

| quote: |

| Originally posted by Lebezniatnikov http://krugman.blogs.nytimes.com/20...s-have-wrought/ |

| quote: |

| Originally posted by Clovis Fuck, thats terrible. The states really need this money... |

My, what a change in tone.

Democrats strike a different tone on Katrina

| quote: |

Democrats strike different tone on Katrina By BEN EVANS � 1 day ago WASHINGTON (AP) � The economic stimulus signed by President Barack Obama will spread billions of dollars across the country to spruce up aging roads and bridges. But there's not a dime specifically dedicated to fixing leftover damage from Hurricane Katrina. And there's no outrage about it. Democrats who routinely criticized President George W. Bush for not sending more money to the Gulf Coast appear to be giving Obama the benefit of the doubt in his first major spending initiative. Even the Gulf's fiercest advocates say they're happy with the stimulus package, and their states have enough money for now to address their needs. "I'm not saying there won't be a need in the future, but right now the focus is not on more money, it's on using what we have," said Sen. Mary Landrieu, D-La., who has criticized Democrats and Republicans alike over Katrina funding. It's a significant change in tone from the Bush years, when any perceived slight of Katrina victims was met with charges that the Republican president who bungled the initial response to the disaster continued to callously ignore the Gulf's needs years later. Just last summer, Democrats accused Bush of putting Iraq before New Orleans when he sought to block Gulf Coast reconstruction money from a $162 billion war spending bill. Bush was pilloried for not mentioning the disaster in back-to-back State of the Union addresses. Former Rep. Jim McCrery, R-La., who helped lead the fight for Gulf aid before retiring last year, said he was surprised over the lack of Katrina money in the bill, but figures lawmakers may be granting Obama leniency due to the magnitude of the country's current economic challenges. "Any new president is going to have a little honeymoon," said McCrery, who is now a lobbyist. "I'd like to think that the tone would have been the same with any new president." Thomas Langston, a Tulane University political scientist, said Democrats may be "playing nice" to keep in good favor. But dire needs remain, he said. "Hopefully they've gotten some promises behind the scenes about longer-term commitments," Langston said. "Like most people down here, I would hate for anybody to get the impression that, 'We're good, thank you.'" The federal government has devoted more than $175 billion to the region since Katrina ripped through New Orleans in 2005, and billions remain unspent. It's unclear how much more money will be needed, but nearly everyone agrees that the federal government should continue investing heavily in the region's levees and other infrastructure to prevent a repeat of Katrina's devastation. Under the $787 billion stimulus bill, states will share more than $90 billion in infrastructure money. Gulf states such as Louisiana, Mississippi and Alabama can use their funds for Katrina-related projects, but they'll get the same formula-based share that other states receive. There was hardly a complaint as Obama and other Democratic leaders pieced together the package. Members of the all-Democratic Congressional Black Caucus, who have called Bush's Katrina funding a moral failure, said they were thrilled with the stimulus. Landrieu won several provisions that do not allocate new money but are aimed at cutting through red tape to free up existing funds. "I think people looked at how generous Congress has been in the past," said Rep. Bennie Thompson, a Mississippi Democrat who chairs the House Homeland Security Committee. "(The states) have to demonstrate that they can be good custodians of the money." Thompson and others say new funding wasn't necessary in the stimulus largely because billions of federal dollars remain bogged down in bureaucracy or tied up in planning. As a result, they said, Katrina funding doesn't fit with the quick-spending purpose of the stimulus bill, which is aimed at kick-starting the economy. Ironically, Bush made similar arguments in recent years as Gulf advocates latched on to nearly any legislation they could find to pursue reconstruction money. For example, he routinely argued that Katrina funding didn't belong in war spending bills and that new funding wasn't urgent because unspent billions were already in the pipeline. In part, the lack of criticism this year could reflect a stronger trust by fellow Democrats that Obama will follow through with his campaign pledge to rebuild levees and "keep the broken promises" to the Gulf. Whether the grace period continues could hinge on how Obama addresses the issue in future spending bills. Without discussing specific funding plans, White House spokeswoman Gannet Tseggai said Obama is "dedicated to rebuilding New Orleans and the Gulf Coast and looks forward to working with Congress to ensure they get the help they so desperately need." |

| quote: |

| Originally posted by Clovis Fuck, thats terrible. The states really need this money... |

I don't understand how that chart correlates with states getting targeted assistance from the stimulus package.

| quote: |

| Originally posted by Clovis I don't understand how that chart correlates with states getting targeted assistance from the stimulus package. |

I don't think that is exactly what is happening, but, thanks.

AFAIK California hasn't been getting money because we haven't been able to pass a budget until 2 days ago. Banks would not lend to the state until we had a budget that showed how we were going to deal with the shortfall.

The money in the stimulus bill would help keep certain programs afloat during the budget crisis, key programs that have been cut or cut back so that the state government could balance and pass a budget.

The idea that banks are refusing to lend is a half-truth. This country is so over-leveraged as is that there is not a lot of demand for credit. Yes, liquidity is sloshing around, but who has the capacity to borrow in these times?

Powered by: vBulletin

Copyright © 2000-2021, Jelsoft Enterprises Ltd.