TranceAddict Forums (www.tranceaddict.com/forums)

- Political Discussion / Debate

-- Obama's economic speech

Obama's economic speech

Let me preface this by saying I'm no economic guru. I included the red meat of what I've read today. A lot of things Obama said today are scary as hell. First of all, this is a classic case of a big-government liberal basically saying our only chance for economic survivial is to rely on government... suprise!

It seems like just a year or so ago that deficit spending was evil, irresponsible, and an attack on America's future. In fact, it was just a year ago, when Democrats and the media excoriated George Bush for cutting taxes to stimulate growth while increasing federal spending after 9/11 and during the war on terrorists. Bush got crushed for deficit spending. Now Democrats and the media cheer as Democrats demand a rate of deficit spending unlike anything seen since World War II:

| quote: |

| The Congressional Budget Office released its latest budget forecast yesterday, and we now really do have red ink as far as the eye can see. Thanks to a 6.6% decline in revenues due to recession, a spending increase of some $500 billion or 19%, and assorted federal bailouts, the U.S. deficit for fiscal 2009 (ending September 30) will nearly triple to $1.19 trillion. That's 8.3% of GDP, which CBO says "will most likely shatter the previous post-World War II record high of 6.0 percent posted in 1983." It certainly blows away any deficit this decade, not to mention the Reagan years when smaller deficits were the media cause celebre. But there's more. None of that includes the new fiscal "stimulus" that President-elect Obama has promised to introduce upon taking office in two weeks. The details aren't known, but Mr. Obama and Democrats have been talking about at least $800 billion, and probably $1 trillion, in new spending or various tax credits and reductions over two years. Toss that in and add more expected bailout cash, and if the economy stays slow the deficit could reach $1.8 trillion, or a gargantuan 12.5% of GDP. That 2006 Democratic vow to pass "pay as you go" budgets seems like a lifetime ago, which in political terms it was. Whether or not you think new spending will stimulate the economy, the one undeniable truth is that this money has to come from somewhere, which means that it is borrowed or taxed from the private economy. This spending blowout is all but guaranteeing huge future tax increases, and anyone who thinks only the rich will pay is living an illusion. Taxpayers need some new champions in Washington- and fast. |

| quote: |

| There are welfare payments for unemployed people, people who don't pay taxes at all, income taxes, and there are business write-offs for businesses that lose money. But there's no tax cuts for people who are stimulating the economy. Who stimulates the economy, by the way? How many deficits have we been running as a nation, budget deficits, annual, for how many years now? And yet this recession still happened. We've already tried this. It was just two months ago that we tried this very circumstance. We have been stimulating the economy in a robust way, according to the way the left defines it, and still Obama tells us it's getting worse, and just like they sold the first $700 billion, "We gotta do it now, we can't wait, it's a crisis, we cannot wait any longer, our country can't afford to wait," and we are being micromanaged and hurried into a blunder of historic proportions. This [plan] is basically printing as much money as humanly possible. Because, we don't have the value to back up the money that we are spending, we're not borrowing as much as we're going to spend. The Chinese have sent out little warning notices saying, "Hey, you know, we may not continue to purchase your debt anymore," and it's a bunch of foreign nations that have been purchasing our debt, T-bills and all that. We're having to print this money, and we are unloading it. We're going to unload this printed money on favored industries and unions and populations to promote left-wing policies and entities, such as the green movement. We're going to hand out massive welfare payments to nontaxpayers, and we're going to call it a middle-class tax cut. If this happens, as envisioned by Obama, this is gonna go down as the biggest economic blunder in American history. The Wall Street Journal has a column today. Obama wants to talk about the Wall Street wrongdoers and so forth? "The Congressional Budget Office reports that some $240 billion of the new spending," bailout money, "is for the bailout of Fannie Mae and Freddie Mac. Congress will also want to keep in business Fannie Mae and Freddie Mac as part of its nationalization of the mortgage market. So that $240 billion to bail out Fannie Mae and Freddie Mac may never be repaid, although only last year our Solons and Treasury Secretary Hank Paulson were ensuring us that Fannie and Freddie were no threat to taxpayers." Fannie and Freddie were no threat to taxpayers, they're fine. Well, we just bailed them out $240 billion and they're not going to have to pay it back. Think of it in Madoff terms. Think of it as Congress having stolen from the taxpayers, as a result of its Fannie Mae scam, nearly five times what Bernie Madoff made, have stolen from his clients. And yet the very people that led to the problem, now fixed it by-- a scam five times the size of Bernie Madoff's, and Obama today says, "No longer can we allow Wall Street wrongdoers to slip through the regulatory cracks." |

I'm tired and not going to take this on right now, but this is an example of why Republicans have been banished to the wasteland right now - they refuse to face the current facts of the economy.

You really think Democrats are applauding the circumstances that make these massive bailouts necessary? You're misplacing your hatred of liberals on this one. We hate these bailouts almost as much as you do (after all, don't you think there are things aka universal healthcare that we'd rather be spending the money on?) - the difference here is that we see the writing on the wall.

| quote: |

| Originally posted by Lebezniatnikov I'm tired and not going to take this on right now, but this is an example of why Republicans have been banished to the wasteland right now - they refuse to face the current facts of the economy. You really think Democrats are applauding the circumstances that make these massive bailouts necessary? You're misplacing your hatred of liberals on this one. We hate these bailouts almost as much as you do (after all, don't you think there are things aka universal healthcare that we'd rather be spending the money on?) - the difference here is that we see the writing on the wall. |

| quote: |

| Originally posted by The17sss Yes, in fact I do think they are applauding it because it furthers the Democrat way of making more and more people feel like government is the only way to make their lives better, which equals more government growth and power and dependency... hence, more votes. You guys destroyed Bush in regards to his out of control spending, and this is even worse, but you're like "give it a chance... let's let this play out... etc." And, I think what's killing the Republicans at this moment right now is that they are hedging their bets and NOT standing up for their conservative principles and against this with megaphones. They are hedging along with Obama (being vague about how long this will last) because that's just the truth: nobody is really sure if it will work out at all. The furthest he'll go is to say he's "confident" it'll "save or create" three million jobs; if you�re wondering what that means in real terms, just pick the number of jobs that you expect will be lost by 2010 and add three million to that. That's how many we'll be told would have been lost if this hadn't passed. It's his own pessimism that explains why he's been so conciliatory towards the GOP: Its not about "changing the tone," it's about knowing that the ship's going down and wanting Republicans on deck with him so that they don't capitalize in the midterms. I don't know man... doesn't it just seem more logical that to stimulate the economy, large tax cutting would be the answer and not depending more and more on government? Their very policies startin with Carter's "community re-investment act" and Clinton doubling down on it in 1995 forcing banks to give even riskier loans is at the root of what we have now with Banks needing bailouts. And the same people/policy supporters of those types of things are the ones coming up with the ideas on how to "fix" this? It's unbelievable to me. |

| quote: |

| Originally posted by Krypton the7sss, we've just had 8+ years of deregulated big business economics which ended up completely dead in the water. And your solution is what? More big business economics? They are currently laying off millions of jobs (2+ million already). What would you have them do? Wallow in the pit? Our country needs extensive infrastructure investment. Hint: Job stimulation. Too bad the current administration thought some third world backwater was worth our blood and treasure, while our infrastructure/economy at home is in disrepair. But what really irks me is people like you (no disrespect) who want more of the same. |

| quote: |

| In 2005, state and local governments collected approximately $40.3 billion in such taxes from motorists for the stated purpose of road construction and maintenance. Out of that $40.3 billion, only $28.5 billion remained available after payment for administrative overhead, i.e., all that lovely government bureaucracy. $1.4 billion was used for mass transit, $7.5 billion was used for social services and another $8.9 billion was diverted to unrelated causes. That leaves only $13 billion, out of the original $40.3 billion we paid the government, that was actually spent on road construction and maintenance. |

| quote: |

| Originally posted by The17sss Yes, in fact I do think they are applauding it because it furthers the Democrat way of making more and more people feel like government is the only way to make their lives better, which equals more government growth and power and dependency... hence, more votes. You guys destroyed Bush in regards to his out of control spending, and this is even worse, but you're like "give it a chance... let's let this play out... etc." |

| quote: |

| And, I think what's killing the Republicans at this moment right now is that they are hedging their bets and NOT standing up for their conservative principles and against this with megaphones. They are hedging along with Obama (being vague about how long this will last) because that's just the truth: nobody is really sure if it will work out at all. |

| quote: |

| The furthest he'll go is to say he's "confident" it'll "save or create" three million jobs; if you�re wondering what that means in real terms, just pick the number of jobs that you expect will be lost by 2010 and add three million to that. |

| quote: |

| "I'd like to see it bigger." Krugman said. "I understand that there's difficulty in actually spending that much money, and I--they're also afraid of the--of the T word. They're afraid of a trillion dollar for the two-year number. But you know, the back of my envelope says it takes roughly 200 billion a year to cut the unemployment rate by 1 percent from what it would otherwise be. In the absence of this program, we could very easily be looking at a 10 percent unemployment rate. So you do the math and you say, you know, even these enormous numbers we're hearing about are probably enough to mitigate but by no means to reverse the slump we're heading into. So this is--you know, I--they're thinking about it straight." |

| quote: |

| That's how many we'll be told would have been lost if this hadn't passed. It's his own pessimism that explains why he's been so conciliatory towards the GOP: Its not about "changing the tone," it's about knowing that the ship's going down and wanting Republicans on deck with him so that they don't capitalize in the midterms. |

| quote: |

| I don't know man... doesn't it just seem more logical that to stimulate the economy, large tax cutting would be the answer and not depending more and more on government? |

| quote: |

| Their very policies startin with Carter's "community re-investment act" and Clinton doubling down on it in 1995 forcing banks to give even riskier loans is at the root of what we have now with Banks needing bailouts. |

| quote: |

| Originally posted by The17sss This whole "infrastructure" argument is a joke... people who believe that are the same ones that buy into the myth that FDR's New Deal saved us from the Great Depression. |

| quote: |

| Originally posted by The17sss 17 times since 2003 Bush tried to put regulation into Fannie and Freddie and was denied by the Dem thiefs who were using it as a personal piggy bank. You seem to forget that. I don't have the link in front of me but I can find it in all it's deatail if you want. Don't confuse regulation/deregulation with piss poor management of such institutions. |

For what it's worth, this is the appraisal of the Obama plan I've been reading about from most Dems:

| quote: |

| Harkin Fears "Trickle-Down" Stimulus By Elana Schor - January 8, 2009, 5:27PM Democratic senators are still emerging from their closed-door briefing with Obama economic adviser Larry Summers ... but a senior Democratic senator, Iowa progressive Tom Harkin, just gave me a dire buzzword: trickle-down. "There's only one thing we've got to do in this stimulus, and that's create jobs," Harkin told me. "I'm a little concerned by the way Mr. Summers and others are going on this ... it still looks a little more to me like trickle-down." Likening Barack Obama's economic recovery plan to the failed supply-side excesses of the Reagan and Bush years is a bit of a Cassandra moment. But Harkin didn't back down. "What I'm hearing from Mr. Summers is that they've got a different approach -- tax breaks, and this and that," he said. Harkin warned that, much like the outcome of George Bush's $600 stimulus package last year, recipients of quick tax cuts "are going to be salting it away, not spending it." When I asked if he felt his concerns were heard during the meeting, he looked to the floor and slowly shook his head. It was almost forlorn. |

| quote: |

| Not Doing Enough by John B. Judis Why I worry that Obama doesn't realize just how bad things are. Post Date Friday, January 09, 2009 Does Barack Obama understand the seriousness of the economic crisis? Yesterday, he laid out his economic agenda, and it was filled with all sorts of important exhortations and proscriptions. He appropriately condemned the "anything goes" policies of the last administration. He declared that government is now the solution to our woes, not the problem. Still, I worry that the president elect is underestimating the problem he and the country faces. We may not simply be facing a steep recession like that of the early 1980s, from which we can extricate ourselves in a year or two, but something resembling the Great Depression of the 1930s. For starters, the current crisis is global, which means that one part of the world can't lift the other out of its misery; everyone will go down together, which is what happened in the 1930s. Secondly, the downturn has combined an unusual decline in the real economy--employment in durable-goods manufacturing fell by 21.9 percent from 2000 to 2008--with a financial crash precipitated by the bursting of the housing bubble. The bubble resulted from an attempt to sustain growth and employment in the face of an underlying decline, which, too, is what happened in the late 1920s. Over the past six decades, policymakers have used some tactics from the Great Depression to quell recessions--such as spending on roads and bridges to create jobs, transferring payments to raise consumer demand, and infusing money into the credit system. But these stopgap measures, which are at the heart of Obama's recovery program, may prove inadequate. There's much to like in Obama's plan. But there are two important ways he may have to go further. Most economists agree that what finally pulled the U.S. out of the Great Depression was military spending for World War II. Some liberals argue that if the Roosevelt administration had not abandoned a Keynesian stimulus strategy in 1937-38, the U.S. might have gotten out of the depression without a war. But in 1936, unemployment was still at 16.9 percent; by 1942, after two years of war spending, it was 4.7 percent, strongly indicating that it was war spending that did it. I am not suggesting that the United States start a world war in order to solve the world's economic problem. But I am suggesting a strategy that could be called the fiscal equivalent of war. It would consist not merely of updating or repairing the nation's infrastructure, but in undertaking massive new investments that would expand the scope of American industry, and address other urgent problems in the process: global warming, over-reliance on petroleum, and the need to revive America's domestic manufacturing capabilities--not just to provide jobs, but also to provide tradeable goods that can reduce the country's current account deficit. One area that is ripe for such investment--and that is not, from what I have seen, a declared priority of the Obama administration--is high-speed rail. Amtrak's Acela trains--the closest thing we have to one--average less than 100 mph between Washington D.C. and Boston, whereas trains in Western Europe and Japan go more than twice as fast. Many of them also run on electricity. They would be the most energy-efficient and quickest means of getting between places like Boston and New York, or Los Angeles and San Francisco. But they would require a massive investment. For instance, installing high-speed rail in the Northeast corridor could cost about $32 billion, while California's high-speed rail system would require up to $40 billion. A system that would address the other areas of the country could easily raise the cost to the hundreds of billions. The House transportation and infrastructure committee has currently proposed $5 billion in stimulus funds for intercity rail--not even a down payment on what it would cost to convert the U.S. to high-speed rail. Investing in high-speed rails would be very expensive, but unlike tax cuts--the benefits of which can be siphoned off in the purchase of imported goods--the money spent would go directly to reviving American industry and improving the country's trade balance. That doesn't just mean jobs creating dedicated tracks or new rail stations: Though the U.S. abandoned train manufacturing decades ago to the French, Germans, Canadians, and Japanese, this kind of production could be undertaken by our ailing auto companies or aircraft companies--if the federal and state governments were to place orders. And building trains that would run on electricity would be a paradigmatic example of the "green jobs" that Obama often touts. Though a massive investment in high-speed rail brings its own set of complications, it's worth keeping these kind of examples in mind when one hears from the Obama people that they can't find sufficient infrastructure projects to fund. The question I would pose is this: Are we not at some point going to have to go beyond repairing roads and bridges in our conception of public spending and public works, and contemplate the kind of ambitious industrial expenditures that the country made on war production in 1941? The second arena that needs radical action from Obama is international. One reason that the depression of the 1930s endured and deepened was because the international monetary system, which had been based on gold, broke down; and one reason that the world economy enjoyed reasonable prosperity between 1945 and 1971 was because the International Monetary Fund--created as part of the Bretton Woods system in 1944--ensured a measure of international monetary stability. Countries controlled their capital inflow and outflow, and the IMF oversaw--if imperfectly--surpluses and deficits, and devaluations and revaluations. Currency exchange was regulated by nations, not by private companies or speculators. And the only country that ran a large surplus after World War II--the United States--took it upon itself to spend much of it helping the other countries to revive their industries. Since 1971, the breakdown of Bretton Woods has given way to a perverse anti-system that combines floating rates, fuelled by speculation, and behind-the-scenes currency manipulation by counties like China and Japan that don't want their exports priced out of foreign markets. The result, as Martin Wolf and others have argued, has been decades of financial crises, which began on the fringes of the system but have now engulfed the center. This system, which features huge surpluses in China and Japan, and huge deficits in the United States, has not proven viable, and is breaking down right now. If China is "losing [its] taste for debt from the U.S.," as a recent New York Times story reported, the U.S. will have trouble financing its deficit expenditures. Interest rates will go up, investment will go down, income will sink, and more Americans will be out of jobs; on the other side of the Pacific, China will be able to sell less goods to the U.S., its investment will fall, its workers will be jobless, and so on. It's not a pretty picture. What's needed, it appears, is a new international system that will prevent the kind of global imbalances that are plaguing the current system. Like Bretton Woods worked initially in practice, it will place the onus of regulating these imbalances on countries running surpluses, not deficits. It would also permit countries to develop economic strategies without fearing that speculators would create a run on their currency. Larry Summers and Tim Geithner are well-suited to work out the details of such broad reform, but Obama has yet to make this a priority within his economic policy. The U.S. also needs to begin working on its own strategy to reduce its current account deficits. That may require not only very large government subsidies to manufacturing industries, but also some currency manipulation of our own to get the price of our goods competitive with those produced in Asia. Obama is certainly right to abandon the "anything goes" mentality of the Bush administration and to promote an $800 billion stimulus program. But to reverse to current economic collapse, the new administration may have to go even farther than this in the direction of a fiscal equivalent of war and a new Bretton Woods. John B. Judis is a senior editor of The New Republic and a visiting scholar at the Carnegie Endowment for International Peace. |

| quote: |

| Originally posted by Lebezniatnikov Absolutely not. It doesn't work and it never has. |

where the fuck is occrider when you need him?

if occrider, renegade, arbiter and moral hazard had a baby together, i reckon the child would grow up to bring about world peace.

| quote: |

| Originally posted by The17sss you can't possibly say that cutting taxes has never worked in stimulating economic growth. are you kidding? |

| quote: |

| Myth 3: The economy has grown strongly over the past several years because of the tax cuts. �The main reason for our growing economy is that we cut taxes and left more money in the hands of families and workers and small business owners.� � President Bush, November 4, 2006 Reality: The 2001-2007 economic expansion was sub-par overall, and job and wage growth were anemic. Members of the Administration routinely tout statistics regarding recent economic growth, then credit the President�s tax cuts with what they portray as a stellar economic performance. But as a general rule, it is difficult or impossible to infer the effect of a given tax cut from looking at a few years of economic data, simply because so many factors other than tax policy influence the economy. What the data do show clearly is that, despite major tax cuts in 2001, 2002, 2003, 2004, and 2006, the economy�s performance between 2001 and 2007 was from stellar. Growth rates of GDP, investment, and other key economic indicators during the 2001-2007 expansion were below the average for other post-World War II economic expansions (see Figure 2). Growth in wages and salaries and non-residential investment was particularly slow relative to previous expansions, and, while the Administration boasts of its record on jobs, employment growth was weaker in the 2001-2007 period than in any previous post-World War II expansion. (http://www.cbpp.org/8-9-05bud.htm) Median income among working-age households, meanwhile, fell during the expansion. Census data show that among households headed by someone under age 65, median income in 2006, adjusted for inflation, was $1,300 below its level during the 2001 recession. Similarly, the poverty rate and the share of Americans lacking health insurance were higher in 2006 than during the recession. (http://www.cbpp.org/8-28-07pov.htm) Myth 4: Even if economic growth and the job market were weak during the early stages of the recovery, the capital gains and dividend tax cuts turned the economy around in 2003. �Since the tax rates on capital gains and dividends were reduced in 2003, we have seen strong steady economic growth, resulting in higher employment.� � Representative Bill Thomas, then Chair of the Ways and Means Committee, May 17, 2006 Reality: The available evidence indicates that the capital gains and dividend tax cuts were not the cause of improvement in the economy in 2003. The President and other tax-cut advocates have credited the capital gains and dividend tax cuts with the fact that the economy performed better between 2003 and 2007 than in the earlier part of the expansion. But they have produced no evidence to support their leap from correlation (the tax cuts coincided with improvement in the economy) to causation (the claim that the tax cuts caused the improvement). Furthermore, they have ignored evidence that indicates there was little or no causal connection. Notably, informed observers such as Federal Reserve Chairman Ben Bernanke (then a Federal Reserve Board governor) were predicting improvement in the economy before the 2003 tax cuts were enacted. In addition, supporters of enacting these tax cuts, such as conservative economist Gary Becker, acknowledged at the time that, whatever the tax cuts� long-run effects on economic growth, they would not boost the economy in the short term. Also striking is the fact that the expansion of the 1990s followed a pattern similar to the 2001-2007 expansion, especially with respect to investment growth (which the dividend and capital gains tax cuts were supposed to encourage). Investment was weak in the early 1990s and then began to improve about two years into the expansion. But in the 1990s, that improvement � which was greater than the improvement in the early 2000s � coincided with a tax increase (see Figure 3). If one accepts the notion that any economic change that follows a tax change must have been caused by the tax change, one would have to conclude that tax increases promote stronger investment growth than tax cuts. The more reasonable conclusion, of course, is that weak recoveries eventually tend to return to historical norms. Moreover, even growth since 2003 has been less than impressive. GDP, wage and salary, and employment growth have remained below average for a post-World War II recovery, while growth in non-residential investment has only matched the historical norm. (http://www.cbpp.org/7-10-07tax.htm) Myth 5: Extending the tax cuts is important for the economy�s long-run health. �To keep this economy growing and delivering prosperity to more Americans, we need leaders in Washington who understand the importance of letting you keep more of your money, and making the tax relief we delivered permanent.� � President Bush, October 28, 2006 Reality: Extending the tax cuts without paying for them would be more likely to reduce economic growth over the long run than to increase it. Researchers at the Joint Committee on Taxation, the Congressional Budget Office, and the Brookings Institution have all found that large unpaid-for tax cuts reduce economic growth over the long run. For example, a study by Brookings Institution economist William Gale and then-Brookings economist (now CBO director) Peter Orszag concluded that making the 2001 and 2003 tax cuts permanent without offsetting their cost would be �likely to reduce, not increase, national income over the long run.� Similarly, in a study in which it examined the economic effects of reductions in individual and corporate tax rates and an increase in the personal exemption, the Joint Committee on Taxation found, �Growth effects eventually become negative without offsetting fiscal policy [i.e. without offsets] for each of the proposals, because accumulating Federal government debt crowds out private investment.� (http://www.cbpp.org/3-19-07bud.htm) The reason behind these results is that, even if tax cuts have modest positive effects on work and savings decisions, those effects are outweighed by the negative consequences of higher budget deficits. In claiming that tax cuts will boost savings, investment, and GDP growth, supporters often seem to forget that national savings has two components: private and public (i.e., government) savings. Tax cuts could positively affect private savings, although, as the Congressional Research Service has noted, studies have failed to find large effects. But when the federal government runs a deficit, it pays for the deficit by borrowing money from the private sector, which reduces national savings. By adding to deficits, unpaid-for tax cuts thus generally reduce national savings. Making the tax cuts permanent would add about $4.4 trillion to deficits over the next decade, when the additional interest costs on the national debt are included. The resulting decrease in national savings would mean fewer funds available for investment, reducing the size of the capital stock (the total supply of equipment, buildings, and other productive capital in the economy). With less capital available, future workers would be less productive, and as a result, national income over the long run would be lower than it otherwise would be. (As discussed above, even if paid for, the positive effects of the tax cuts on the economy would be quite small. Moreover, paying for the tax cuts with spending cuts would require deep cuts in federal programs, as discussed below in Myth 8.) |

that is the biggest bunch of bullshit I've ever read. So much of those theories are conditional and dependant on several variables... if you truly believe the best way to spark investment, entrepreneurism, and consumer confidence is to raise taxes, you're the one in la la land. By your rationale, we should tax the living shit out everyone and everything for a reeeeeally sound economy. It is precisely times like that (when taxes are raised) when the wealthy who invest and those to create job opportunities in the private sector hold on tighter to their money and lay people off to cut costs.

| quote: |

| Originally posted by The17sss that is the biggest bunch of bullshit I've ever read. So much of those theories are conditional and dependant on several variables... if you truly believe the best way to spark investment, entrepreneurism, and consumer confidence is to raise taxes, you're the one in la la land. By your rationale, we should tax the living shit out everyone and everything for a reeeeeally sound economy. It is precisely times like that (when taxes are raised) when the wealthy who invest and those to create job opportunities in the private sector hold on tighter to their money and lay people off to cut costs. |

Lower taxes are only good when money isn't BORROWED to lower them.

That's what I got out of the article..and it is absolutely true. If you reduce taxes while increasing the deficit, the burden is only shifted around to other areas. The national debt will increase and the currency will be devalued, so people end up being hurt just as much (if not more) than they would have been with a higher tax rate and balanced federal budget (+ stronger currency).

| quote: |

| Originally posted by Lebezniatnikov Whoa there, that's not what it said. It said if one is to truly believe that economic growth is contingent on tax policy alone, that is the only valid conclusion. Therefore the relationship between growth and tax policy is probably not as strong as we thought. That's all it said - it didn't advocate raising taxes; it merely pointed out that logically, if you really believed tax policy was the sole cause of economic growth or decline, that raising taxes would be the more valid conclusion. |

Krugman has been writing a lot about how the current Obama plan probably isn't enough:

| quote: |

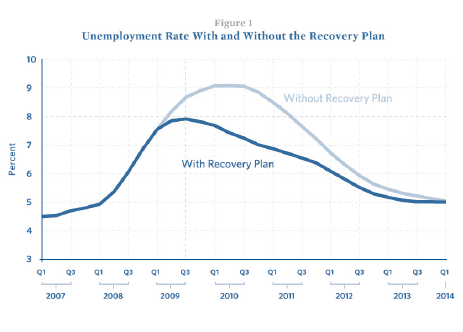

| Romer and Bernstein on stimulus OK, Christina Romer and Jared Bernstein have put out the official (?) Obama estimates of what the American Recovery and Reinvestment Plan would accomplish. The figure above summarizes the key result. Kudos, by the way, to the administration-in-waiting for providing this � it will be a joy to argue policy with an administration that provides comprehensible, honest reports, not case studies in how to lie with statistics. That said, the report is written in such a way as to make it hard to figure out exactly what�s in the plan. This also makes it hard to evaluate the reasonableness of the assumed multipliers. But here�s the thing: the estimates appear to be very close to what I�ve been getting. The key thing if you want to do comparisons is to note that I made estimates of the average effect over 2009-2010, while they do estimates of effect in the fourth quarter of 2010, which is roughly when the plan is estimated to have its maximum effect. So they say the plan would lower unemployment by about 2 percentage points, I said 1.7, but their estimate may actually be a bit more pessimistic than mine. They have the plan raising GDP by 3.7 percent, but that�s at peak; I thought 2.5 percent or so average over 2 years, again not much difference. So this looks like an estimate from the Obama team itself saying � as best as I can figure it out � that the plan would close only around a third of the output gap over the next two years. One more point: the estimate of what would happen to the economy in the absence of a stimulus plan seems kind of optimistic. The chart above has unemployment ex-stimulus peaking at 9 percent in the first quarter of 2010 and coming down through the year; the CBO estimates an average unemployment rate of 9 percent for 2010, so the Obama people are more optimistic than the CBO, and a lot more optimistic than I am. Bottom line: even if I use the Romer-Bernstein estimates instead of my own � there really isn�t much difference � this plan looks too weak. |

| quote: |

| What to Worry About There's a lot of empirical evidence and a lot of very knowledgeable people who believe the Obama Stimulus Plan (the general outlines of which are coming into focus) is simply not big enough -- not only in overall dollar size but also in the kinds of spending included in it. Paul Krugman has been posting on the issue at his blog, particularly in this post. And this article in the Times covers it more broadly. http://www.nytimes.com/2009/01/10/w...&pagewanted=all The debate about spending priorities essentially comes down to how much bang for your buck you get in economic stimulus terms for tax cuts or rebates (even for middle or low income people most inclined to spend it) versus government spending, especially in the context of a dramatic economic downturn. And from what I can tell there's a lot of empirical evidence that the latter wins out by a substantial margin. And yet the desire to get a substantial number of Republicans to vote for the bill appears to be having a big impact on the proposal's size and shape. Quite likely, leaving it too small and too tilted toward tax cuts to get the job done. Late Update: Nate Silver has an interesting and at least partly persuasive political interpretation (thanks to TPM Reader EW for flagging it for me) of what's going on here: namely, that Obama is trying to start low and let the bidding run higher, leaving it mainly to the Senate Dems to do the heavy lifting of bidding the thing up. Remember, Obama himself did seem to hint at such a strategy earlier last week. http://www.talkingpointsmemo.com/ar...l_and_build.php If we assume for the sake of the conversation that this or something like it is Obama's strategy, my reaction is two-fold. First, the legislative process is always messy. But this is a case where you want it to be as little messy as possible. We're spending a staggering amount of money here -- and for both political and policy reasons, you want it to be focused, efficient (in terms of delivering stimulus) and focused on spending projects that will not only employee people in the medium term but spur efficiencies, economic growth and other good things for the long term. If you get deep into a lot of bidding and horse-trading you get more parochial interests in the mix which cuts against those goals. I don't say that makes it a bad idea necessarily. But it's a real concern. Second, when I write stuff critical of Obama, either on the policy or political fronts, there's always a rush of emails saying, 'Give him a chance!' 'Leave Obama alone!' 'He's probably got a plan you don't know about!' and so on. He may. I hope he does. But all of these debates are dynamic. You never assume anything. If Nate's right about what Obama's plan is, having people pushing for something better from the outside is part of it. So under either scenario, holding your tongue makes no sense, in addition to being unethical. Final Saturday Night Update: Here's a piece from the Post about concerns about the make-up of the bill. --Josh Marshall |

Here's a post by Digby pertaining to a show on CNN called "I.O.U.S.A." to which I think his reply to the show is relevant to the discussion (emphasis mine below):

| quote: |

| Americans have been mentally trained over the past few decades to believe drivel like that--- the free market is always the preferred method to solve economic problems, that the government should be run like a business (or your household budget) and, most importantly, that government is the cause of problems, not the solution. This deficit obsession plays into all those beliefs and makes it very difficult to explain in the middle of the crisis that the government isn't a business or a household and needs to go further into debt in periods when everyone else is trying to escape it. And, needless to say, it also sounds like the tax 'n spend libruls are at it again. I'm sure it hasn't escaped anyone's notice that the deficit scolds are coming out of the woodwork now that the Republicans brought us to the brink, slashing taxes for the wealthy, larding their own contributors with earmarks, solidifying the notion that military industrial complex spending is a sacred, untouchable icon, and fetishing and deregulating the market until they finally brought the whole system to its knees. They certainly didn't say much about the debt while it was adding up these last eight years. They did the same thing during the 80s, which is why Cheney uttered "Reagan proved deficits don't matter. (What was left out was "for Republicans." Democrats are endlessly and relentlessly harassed about deficits --- as they clean up the big mess the deficit spending Republicans leave behind.) They've reanimated the yellow peril, which is only fitting. Last time, we were told that Japan was taking over the country by buying up all of our real estate. This time it's the Chinese buying up all our bonds. (In 92, Perot put a little zesty mexican salsa in the recipe.) It's always something. The foreigners are going to kill us in our beds unless we cut social security and medicare. And if we even think of enacting any new "entitlements" (a conservative buzzword designed to make you think people are getting something they don't really deserve) it's pretty clear that the Asian hordes are going to destroy our way of life (if the muslims don't get to us first.) One of the fundamental characteristics of shock doctrine economics is extreme complexity for which a simple, intuitive solution is proposed. It's hard to argue with and it's hard to resist. Here are famous people who really seem to understand what's going on and the solutions they propose just seem like common sense. Even Joe the plumber can see how right their view is. Unfortunately, they're completely wrong --- at least if you care about the country as a whole and the suffering of the millions of people who will have to endure their "solutions." It's highly unlikely that they will fully have their way on this. We are in deep shit and there are a lot of very smart people who know the deficit is the least of our problems at the moment and that "entitlement reform" is one sure way to deepen the panic and make personal spending contract further than it needs to. (There's a lot of wealth among seniors and near seniors. I can't imagine that chit-chat about how social security is going broke is particularly good news to people who've just lost a good portion of their portfolios in the real estate plunge and the stock market crash.) But these people are going to cause trouble, which comes as no surprise to me. I've been writing about this for years. It's one of the reasons why I believe in liberal rhetoric (and, yes, the dreaded "ideology.") If you don't bother to educate people counter to the myths and propaganda they hear from the right, they have nothing to hold onto except faith in the Democrats in the face of arguments that have been built layer by layer over many years. (And having faith in Democrats really take courage.) The fact that they refuse to do this doesn't automatically spell failure for democratic policies, but it makes it many times harder to succeed. They don't even seem to intend to do tank the stimulus, just restrict it. What they are doing is setting the stage for entitlement cuts and a swift, premature pullback on government spending --- thus extending the crisis. And if the Democrats are cowed by these people (they always are --- they hate being called spendthrifts) there will be enough egomaniacs in the congress to hamstring the administration and force them to adopt these "common sense" methods of running the economy --- which is precisely how we got into this problem in the first place. http://digbysblog.blogspot.com/2009...nt-believe.html |

Just read a pretty down to earth opinion column from John Stossel about Obama's economic plan... makes some good points.

| quote: |

| Arrogant Conceit: Obama Thinks He Can Reform The Economy Barack Obama wants to use the recession to remake the U.S. economy. "Painful crisis also provides us with an opportunity to transform our economy to improve the lives of ordinary people," Obama said. His designated chief of staff, Rahm Emanuel, is more direct: "You never want a serious crisis to go to waste" (http://tinyurl.com/5n8u58). So, they will "transform our economy." Obama's nearly trillion-dollar plan will not merely repair bridges, fill potholes and fix up schools; it will also impose a utopian vision based on the belief that an economy is a thing to be planned from above. But this is an arrogant conceit. No one can possibly know enough to redesign something as complex as "an economy," which really is people engaging in exchanges to achieve their goals. Planning it means planning them. Obama and Emanuel want us to believe that their blueprint for reform will bring recovery from the recession. Yet, we have recovered from past recessions without undertaking a radical social and economic transformation. In fact, reform would impede recovery. This is not the first time a president chose reform over recovery. Franklin Roosevelt did it with his New Deal, and the result was long years of depression and deprivation. Roosevelt's priorities were criticized not just by opponents of big government but by none other than John Maynard Keynes, the British economist whose theories rationalized big government. Before FDR had been in office a year, Keynes wrote him an open letter, which was printed in The New York Times: "You are engaged on a double task, Recovery and Reform; -- recovery from the slump and the passage of those business and social reforms which are long overdue. For the first, speed and quick results are essential. The second may be urgent, too; but haste will be injurious. ... [E]ven wise and necessary Reform may, in some respects, impede and complicate Recovery. For it will upset the confidence of the business world and weaken their existing motives to action. ... Now I am not clear, looking back over the last nine months, that the order of urgency between measures of Recovery and measures of Reform has been duly observed, or that the latter has not sometimes been mistaken for the former." Note Keynes's concern. Government interventions, such as the cartelizing of industry through the National Recovery Administration, "will upset the confidence of the business world and weaken their existing motives to action." In other words, investors will not take the risks necessary for recovery if their profits and freedom are subject to unpredictable government action. Economic historian Roberts Higgs calls this phenomenon "regime uncertainty." Keynes's letter apparently had little influence on Roosevelt, who stuck to his plan. In his second inaugural address a few years later, FDR feared that signs of recovery had jeopardized his reform plans by removing the sense of emergency: "To hold to progress today, however, is more difficult. Dulled conscience, irresponsibility and ruthless self-interest already reappear. Such symptoms of prosperity may become portents of disaster! Prosperity already tests the persistence of our progressive purpose." What a shame. Free people enjoying their lives make it harder for the administration to forcibly impose its utopian vision on them. Obama wants to act quickly. In the name of stimulating the economy, he plans to spend hundreds of billions of dollars the government does not have to convert the economy from carbon-based fuels to "green" alternatives. Even if that were a good idea -- and it's definitely not -- it would not bring recovery. Any money the government spends must be taxed, borrowed or conjured out of thin air by the Federal Reserve, and that will reduce sound private investment. Obama has no real wealth to inject into the economy. He can only move around existing money while inflation robs us of purchasing power. Meanwhile, private investors who might have produced a better engine, battery, computer, cancer treatment or other wealth-creating and life-enhancing innovations, hold back for fear that big government will undermine productive efforts. The way to a lasting recovery is to greatly lighten the burdens of government. Then free Americans will save and invest. Grand interventionist reforms go in precisely the wrong direction. |

Oh Lord. You're quoting Stossel now? He's about as mainstream as Ron Paul. In fact, they're practically peas in a pod.

Powered by: vBulletin

Copyright © 2000-2021, Jelsoft Enterprises Ltd.