|

|

|

|

|

occrider

Traveladdict

Registered: Oct 2000

Location: New York

|

|

|

Ok well PK was a somewhat correct in that your initial response didn't really answer my questions, but your subsequent response to his post gives me some understanding of what your position is.

| quote: | Originally posted by Capitalizt

I said that I preferred fiscal stimulus that focuses on tax relief over expanded welfare programs.

|

With respect to fiscal stimulus, I think I would disagree with you in terms of concentration of fiscal stimulus, however it seems that you accept that all forms of fiscal stimulus: infrastructure spending, social services spending, and tax cuts are all necessary. I think I might disagree with you with respect to the understanding that I think that social services spending (unemployment, welfare, etc.) are absolutely required since they are universally regarded by economists as automatic stabilizers in the business cycle (they tend to smooth erratic swings in consumer spending and thus minimize recessionary troughs).

The second area I might disagree with you is that I think that tax cuts, whilst having a faster velocity to impact (a reduction in payroll taxes can happen in a few weeks or months) are less effective than spending increases particularly in recessions such as this. The reason why I say this is because with every dollar spent in feral spending, you are guaranteed a dollar increase in GDP, with every dollar spent in federal spending, tax cuts do not follow that same parameter because consumers have the option to SAVE money. As such a dollar of fiscal stimulus in tax cuts may well result in less than a dollar in GDP growth. The problem with the tax cuts of last year was that it was estimated that 2/3rds to 4/5ths were not spent at all. Money not spent in fiscal stimulus is money wasted. If one were to look at the fiscal stimulus multiplier, the most effective forms of fiscal stimulus are social welfare programs (a no brainer because people will always spend money rather than starve) and infrastructure projects. What is particularly alluring about infrastructure projects is that the ALSO contribute towards long term growth in GDP.

Btw, in a studies done by moody's you can see their forecasted multiplier impacts for fiscal stimulus components:

http://www.economy.com/mark-zandi/d...ess_7_24_08.pdf

| quote: |

I thought I explained my opposition to almost every aspect of the bailout, including everything the fed has done in the past 12 months. All of the programs oc mentioned have done essentially the same thing (drastically increase the money supply). This is only postponing the inevitable. Things need to correct, and the only alternative is temporary prosperity bought by trillions in additional debt and the destruction of the dollar. Let the market correct. It will be ugly, but it is the lesser of two evils. |

And this part of your argument i disagree the most strongly against. Unfortunately I'll have to address this argument over the weekend. Cheers!

___________________

Retro ...

|

|

Feb-05-2009 07:16 Feb-05-2009 07:16

|

|

|

|

|

Dupz

Supreme tranceaddict

Registered: Dec 2002

Location: Melbourne

|

|

|

| quote: | Originally posted by jerZ07002

the common misconception among people is that high capital gains taxes prevents investment. This idea is ridiculous because people would rather have their money earn 70% (assuming a 30% tax rate) of their gain, than 0% of no gain. The impediment caused by a high capital gains rate is that sometimes people with gains that would be taxed at the capital gains rate may not move their investments because they don't want to pay taxes on that gain. However, there is only a taxing preference if the capital asset is held for a long term (> 1 year), which means assets with rate preferences can't be flipped, and must be held for a period over which that person will likely recapture the lost taxes by a higher return (which is the entire purpose for making a new investment). Admittedly, there is a small impediment to the movement of capital by higher rates, however, it also means new investments will be more highly scrutinizes, which means the money likely will be invested in the most economically efficient manner.

Example:

(1) asset currently appreciates 5% annually, and you have a 100 gain recognized on the sale of the asset

(2) 15% tax on gain is $15, and at 30% is $30.

(3) new asset appreciates 10% annually. It would only take 3 years to recover that difference with the excess return on appreciation (the extra 5% return on asset).

The entire point of preferential rates is that the asset is held for a long period (thus the incentive are actually in line with congressional purpose), and it furthers the most efficient use of capital. |

not sure if i agree with you.. a 30% tax indeed hinders investment (albeit not all of it - but definitely some of it). Any imposed taxes raise the opportunity cost of a transaction.

Hypothetically, if you were to expect a 10% gross yield on an investment and were taxed 30% of it your net yield is 7%. If the risk free rate of return were 8% you would have a disincentive to invest in a more productive venture, because you can make more money with zero risk.

It's a simplistic idea, but taxes hinder those on the margin.

___________________

A witty saying proves nothing.

-Voltaire

|

|

Feb-05-2009 10:30

|

|

|

|

|

Dupz

Supreme tranceaddict

Registered: Dec 2002

Location: Melbourne

|

|

|

| quote: | Originally posted by occrider

With respect to fiscal stimulus, I think I would disagree with you in terms of concentration of fiscal stimulus, however it seems that you accept that all forms of fiscal stimulus: infrastructure spending, social services spending, and tax cuts are all necessary. I think I might disagree with you with respect to the understanding that I think that social services spending (unemployment, welfare, etc.) are absolutely required since they are universally regarded by economists as automatic stabilizers in the business cycle (they tend to smooth erratic swings in consumer spending and thus minimize recessionary troughs).

|

We never focused much on Keynesian economics at school. We viewed depression/expenditure model economics more as economic history, rather than something of practical use. funny that..

I dont think its something to be feared, per se, but i'm thinking that many people will swing too far onto the wrong side of the political spectrum. Protectionism is back on the rise and these people are receiving their 15 minutes - rather than the argument being about legitimate attempts at blunting an economic trough.

A question i'll throw out there: Why do we focus so much on smoothing the negative risks of an economy, but when those exact risks present themselves on the positive side we we worship our obvious intellect and kiss our own asses?

lol, speaking of automatic stabilisers .. i created the damn wikipedia page on them.

___________________

A witty saying proves nothing.

-Voltaire

|

|

|

Feb-05-2009 10:56

|

|

|

|

|

Capitalizt

Supreme tranceaddict

Registered: Feb 2005

Location: USA

|

|

|

| quote: | Originally posted by occrider

I think I might disagree with you with respect to the understanding that I think that social services spending (unemployment, welfare, etc.) are absolutely required since they are universally regarded by economists as automatic stabilizers in the business cycle |

Ah, but when you realize the "business cycle" is not a natural market phenomena in modern economies but a side effect of government intervention and liberal credit expansion policies by the fed, the need for those programs would be greatly lessened. I've realized the errors of going to a pure gold standard and don't agree completely with the articles below, but I do think if we had a fed/treasury intent on reducing intervention and maintaining a stable currency, the economy would tend to balance much closer towards equilibrium over time, and many of the painful "busts" could be eliminated. I've realized the errors of going to a pure gold standard and don't agree completely with the articles below, but I do think if we had a fed/treasury intent on reducing intervention and maintaining a stable currency, the economy would tend to balance much closer towards equilibrium over time, and many of the painful "busts" could be eliminated.

recommended reading: http://mises.org/story/3127

and give these books a go when you find a few months (lol):

http://blog.mises.org/archives/005833.asp

http://www.mises.org/rothbard/agd/contents.asp#contents

| quote: |

The second area I might disagree with you is that I think that tax cuts, whilst having a faster velocity to impact (a reduction in payroll taxes can happen in a few weeks or months) are less effective than spending increases particularly in recessions such as this. The reason why I say this is because with every dollar spent in feral spending, you are guaranteed a dollar increase in GDP, with every dollar spent in federal spending, tax cuts do not follow that same parameter because consumers have the option to SAVE money. As such a dollar of fiscal stimulus in tax cuts may well result in less than a dollar in GDP growth. The problem with the tax cuts of last year was that it was estimated that 2/3rds to 4/5ths were not spent at all. Money not spent in fiscal stimulus is money wasted.

|

ah, here is where we hit the philosophical disagreement. You are correct in all of your math and everything you said here, with one exception. Money not spent in fiscal stimulus is not "wasted" because it was not the government's to begin with. It was already stimulating the economy in private hands. It remains untaxed in the hands of productive private enterprise. It remains in the hands of those who were already benefiting the economy by virtue of being productive enough for the government to tax them. If government refuses to spend their money, they become invisible beneficiaries of the government's refusal to confiscate their wealth. Once again however, we can't point to them and show what investments they will make or people they will hire with the wealth that wasn't taken from them..however I believe those benefits will exceed whatever central planners had in mind for the money. Even if people choose to save money, it can be a great benefit to others (banks in particular). Any studies on what happens when the government refuses to intervene or tax are flawed in my view, because it is impossible to know the full benefits to our economy of not taxing people in the first place. Those benefits are mostly invisible which makes the true multiplier impossible to calculate, while the benefits of spending programs are always obvious and easy to quantify.

Last edited by Capitalizt on Feb-05-2009 at 21:51

|

|

|

Feb-05-2009 14:01

|

|

|

|

|

Lebezniatnikov

Stupidity Annoys Me

Registered: Feb 2004

Location: DC

|

|

|

Another danger that isn't oft reported:

| quote: | About that deflation risk

Look out below

There has been a distinct change in tone from the Obama team today, as they seem to have become suddenly aware that theres a real risk that the stimulus plan will either fail to pass, or be emasculated to the point that it doesnt come close to doing the job. Obama himself has warned of catastrophe if we fail to act, and finally! denounced the tax-cut philosophy. Meanwhile, Larry Summers has finally made the point Ive been pushing for a while that were at major risk of falling into a deflationary trap.

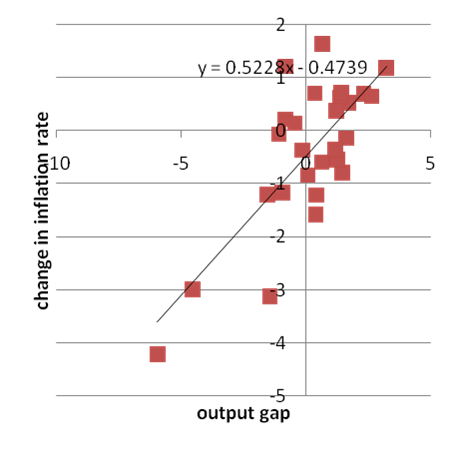

I thought it might be useful to present a bit of evidence behind that concern. The figure above plots an estimate of the output gap the difference between actual and potential GDP, as a percentage of potential and the change in the inflation rate. Both series are taken from the IMF WEO database, for convenience, and use data from 1980-2007.

Its not a perfect fit this is economics, not physics, and anyway stuff besides the output gap bounces inflation around from year to year. But still, theres a clear correlation, driven largely but not entirely by the deep slump and disinflation of the early 1980s, and an implied slope of about 0.5 that is, every percentage point by which real GDP fall short of potential tends to reduce the inflation rate by about half a point over the course of the year.

And right now the CBO is saying that in the absence of a policy action the average output gap will average 6.8 percent over the next two years. Do the math: if anything like the historical relationship between output and inflation holds, were looking at major deflation.

OK, maybe that relationship wont hold getting to actual deflation may take a deeper slump than merely reducing the inflation rate. And maybe a regression driven in part by 80s data isnt a good guide to current events. But deflation is a huge risk and getting out of a deflationary trap is very, very hard.

We truly are flirting with disaster.

|

http://krugman.blogs.nytimes.com/

___________________

|

|

Feb-05-2009 18:07

|

|

|

|

All times are GMT. The time now is 01:37.

Forum Rules:

You may not post new threads

You may not post replies

You may not edit your posts

|

HTML code is ON

vB code is ON

[IMG] code is ON

|

|

|

|

|

|

Contact Us - return to tranceaddict

Powered by: Trance Music & vBulletin Forums

Copyright ©2000-2026, Jelsoft Enterprises Ltd.

Privacy Statement / DMCA

|

More disingenuous nonsense from you

More disingenuous nonsense from you