|

TranceAddict Investors Club @ Marketocracy (pg. 33)

|

View this Thread in Original format

| atbell |

| quote: | Originally posted by Krypton

The student loan industry have very positive growth trends that won't stop because of a mortgage market slowdown.

|

Your risk in the student loan industry is that people start realizing the return on investment just isn't there and that debt is a bit of a crushing obligation.

The reason I'd speculate that education returns might be brought into question is because quality of the North American system has been slidding for a long time now while the cost has been increasing significantly.

I'd also hazard a guess that student loan repayment is not clear of the mortgage market slowdown. If people with student debt, credit card debt and mortgage debt begin to feel financial pressure I'm assumeing the first obligation that goes into default is the student loan. On the other hand if students are graduating with 40 - 80 k worth of debt, if they are rational (:toothless), they wouldn't assume property debt.

Haveing said that, I agree that G & S is worth watching. |

|

|

| Krypton |

| quote: | Originally posted by atbell

Your risk in the student loan industry is that people start realizing the return on investment just isn't there and that debt is a bit of a crushing obligation.

The reason I'd speculate that education returns might be brought into question is because quality of the North American system has been slidding for a long time now while the cost has been increasing significantly.

I'd also hazard a guess that student loan repayment is not clear of the mortgage market slowdown. If people with student debt, credit card debt and mortgage debt begin to feel financial pressure I'm assumeing the first obligation that goes into default is the student loan. On the other hand if students are graduating with 40 - 80 k worth of debt, if they are rational (:toothless), they wouldn't assume property debt.

Haveing said that, I agree that G & S is worth watching. |

Government students loans have taken a cut, noted by a reduction in subsidies to lenders like Sallie Mae. Meanwhile, private student lenders are filling in the void left by the government. Additionally, projected growth rates of student loans is expected to continue going up. There is absolutely no shortage of people going to college because of a subprime mortgage crisis.

In my own experience, every university I've visited is filled to the brim with students. Going to USF, I couldn't find a seat in the damn library. Point, the college growth trend is so obvious, it makes student lenders like FMD, with good fundmentals, a HUGE value investment potential.

I totally disagree with your guys' view of FMD. I think you may be right short term. Long-term, follow the trend. We'll see whose right in time..:o |

|

|

| Krypton |

Why FMD is still a good company despite downgrades and fall in stock price. I can't say it any better than this guy. FMD is a diamond in ruff selling very very cheap values.

| quote: | FBR's Latest First Marblehead Downgrade Makes No Sense

posted on: November 28, 2007 | about stocks: FMD

Allow me to state the obvious, and observe that financial services stocks are in the midst of a painful bear market. To put a number on it that in some ways understates the damage thats been done, the S&P Financials have fallen by 22% in just five months; many individual names are off by much more than that.

And as bear markets go, this ones a classic. In this version, as in all bear markets, fear is investors default emotion. Regardless of the new piece of news or analysis that emerges, investors wont fail to interpret it in the worst possible lightand will keep on selling. This is of course the mirror image of what happens during bull markets, when new news tends to be perceived as positive, and investors send stock prices to levels that, only in retrospect, turn out to be unsustainably high.

When fear is the dominant emotion, often negative media stories and bearish analyst reports can have unusually large short-term downward impacts on stock prices--just like bullish stories and analyst comments have an inordinately positive impact during bull markets.

But in both cases, the overreaction doesnt become clear until time has passed. Go back for a moment to the last sustained bear market in financials, in the late 1980s and early 1990s, and youll see what I mean. In October of 1990, after bank stocks had been going straight down for five years in a row, news emerged that Warren Buffett had accumulated a position in Wells Fargo that added up to 10% of the entire company.

Seventeen years on, its obvious that word of Buffetts Wells holding is about as bullish a piece of news as investors might hope for. At the time, though, people simply didnt see it. Heres what Barrons John Liscio had to say in his Trading Points column on October 29th: Buffett wont have to worry about who spends his fortune much longer, not if he keeps trying to pick a bottom in bank stocks.

Sure enough, the week prior to Liscios comments had brought more dismal performance by bank stocks, and came on top of a harrowing few months that saw many key names fall by 50% or more. But soon enough--on November 1, 1990, to be exact--the stocks began an incredible bull market that lasted for years. For the record, Buffett paid $1.90 each for his shares on a split-adjusted basis. They lately trade around $30. Warren Buffetts investment in Wells Fargo is up by a factor of fifteen!

My point: its easiest to be the most negative on a company after its stock has been falling for an extended period, just as its easiest to be extremely positive after its had an extended bull run. You dont need to have an advanced degree in psychology to understand why, either. Investor fear maxes out when stock prices make new bottoms, just as greed goes into overdrive at tops. At market extremes, investors become overly sensitive to what, they find out later, is mere noise.

All of which is an introduction to my take on FBR analyst Matt Snowlings negative report on First Marblehead (FMD) Monday. In his note, Snowling raised two concerns about the company and downgraded the stock to underperform from market perform. This being a bear market the downgrade had a predictable effect: in a market that was down 2.3% Monday, and in which the S&P Financials Index fell by 4.0%, First Marbleheads stock lost 10%.

Snowlings first concern is that hes worried that credit losses on student loans Marblehead securitized from 2004 through 2006 are running well above expectations, to the point that theyll exhaust the reserves of the loans guarantor, The Education Resource Institute (TERI). Second, he raises the same worry he highlighted back in August, which is that the credit markets are so challenging at this point that Marblehead will not be able to do a planned securitization in the fourth quarter, which would mean that its earnings this quarter will be disappointing.

I happen to emphatically disagree with Snowlings first point, and am unconcerned about his second. As to the companys ability to do a deal anytime soon, first of all, a delay wont affect the long-term business value of the companys franchise unless you believe a complete shut down of the credit intermediation process will continue indefinitely. As to possible higher-than-expected losses on those 2004 through 2006 deals, his numbers are simply wrong, as Ill show in a minute.

I dont think Snowling has intentionally written a research report that is analytically faulty. But I do believe that, because were in the midst of a bear market, investors (both long and short) have accepted his conclusions too quickly, without giving them adequate thought. In my book, this is the classic bear market overreaction--so lets take a closer look at what Snowling had to say.

Im not going to spend a lot of time discussing whether First Marblehead will or wont get a deal done before year-end because, as I say, the issue doesnt bear on the companys long-term value, unless you assume that the current credit market freeze lasts a long, long time. Frankly, thats not a big concern of mine, since 85% of the bonds issued in prior securitizations have been rated AAA and all tranches have performed at or better than expected. As far as that goes, soon after the last time Snowling raised this issue, back in August, Marblehead sold its biggest deal ever.

But with respect to Snowlings comments on student loan defaults, losses, and lack of reserves at the TERI, his analysis is simply way off base, and needs to be addressed.

You can imagine the ramifications that unexpected credit problems could have on Marbleheads ability to generate earnings and cash flow. For starters, a TERI default would immediately impair the value of the residuals on Marbleheads balance sheet. In addition, higher-than-expected credit problems would likely hurt Marbleheads ability to facilitate student loans in the future and then securitize them.

All of which would be very concerning, clearly. Only, if you walk through Snowlings numbers, youll come to the exact opposite conclusion. Defaults are not likely to be the big problem for TERI that Snowling says. And not for a particularly complicated reason, either. Snowling has simply miscalculated a key number: recovery rates for loans already in default.

Ill run through some numbers, and youll see what I mean. Snowling has gone through the nine trusts Marblehead has issued since it began securitizing in 2004, through 2006. He sees no problems for TERI with four of those, but does see potential credit risks for the other five. Lets look at one of those five, the first public trust Marblehead sold, 2004-1; its the most seasoned and thus most likely to be the best indicator of future performance of all the trusts.

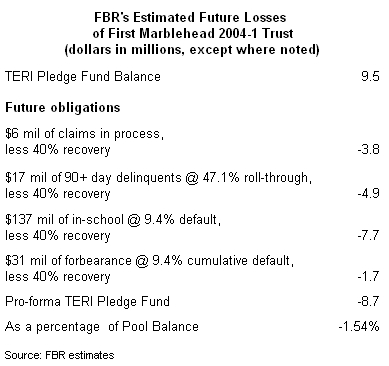

Snowling says that when all is said and done, the 2004-1 trust will generate losses of $8.7 million in excess of the $35.2 million pledge fund that TERI set up to guarantee the bonds at time of sale. Here are his numbers:

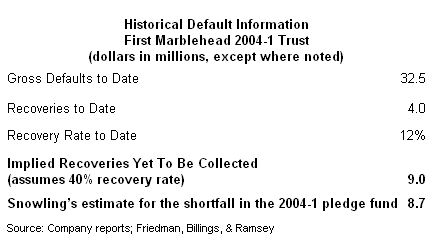

So if you tally up future losses from current delinquencies that go bad at some plausible rate, plus loans now in forbearance that default at some plausible rate, and so forth, and add those losses to the $28.5 million in defaults the trust has already experienced, the TERI pledge fund will end up $8.7 million in the hole.

Theres just one problem with all this. Take a look at Snowlings table again. Note how he assumes a 40% recovery rate in future defaults. Thats in line with the assumptions that TERI and Marblehead made at the time of the trust sale, and is actually conservative compared to Marbleheads own experience. But when Snowling adds in the trusts actual historical losses to date, he assumes that the recovery rate the trust has experienced so farwhich is all of 12%wont rise over time.

Which is, in a word, crazy. TERIs 12% recovery rate on existing defaults is almost certain to rise to the 40% that Snowling assumes for future defaults.

Ill explain why in a minute. But first, a little background. The default-recovery process in private student lending is very, very different than it is in other types of consumer lending. The process can take years. In auto lending, by contrast, when the borrower defaults, the car gets repossessed, and the lender might sell it a few weeks later. The recovery proceeds are in hand before you know it. In mortgage lending, the process takes a bit longer, but isnt likely to last much more than 18 months.

But student lending doesnt work that way. In student lending (which is unsecured, dont forget), experience shows that material recoveries take place over several years following the default. You probably dont have trouble figuring out why, either. For starters, many delinquent borrowers will eventually apply for a mortgagethe first ones might just four or five years after they graduate--and will want to get that student loan derogatory off their credit files in order to get their loan. Or a borrowers earnings power will eventually rise (over four or five years, say) to the point where he can service the loan without much financial strain. For whatever reason, recoveries take place over many years. Remember, the loans are not dischargeable in bankruptcy, so theres never a time when its not worth the lenders time and effort to keep dunning.

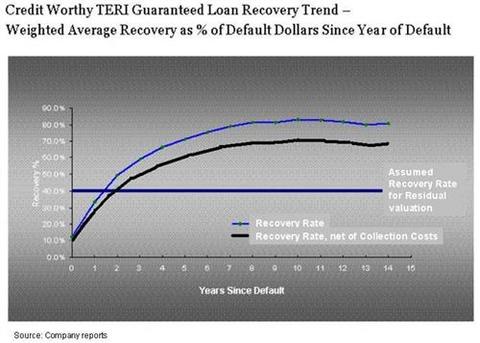

Someone please send Snowling the chart below, which is taken from a recent Marblehead investor presentation. It not only shows the long duration of recoveries on private student loan defaults, it also shows that, while Marblehead assumes a 40% recovery rate at time of securitization, the companys actual experience has been considerably better than that. Net of cost to collect, Marbleheads historical recovery rate is more like 60%!

So when Matt Snowling assumes that the 12% recovery rate of 2004-1 trust wont rise over time, hes making an assumption that isnt just unreasonable. Its idiotic. Material recoveries on 2004-1 will take place over the next several years.

And if you go back and plug in a 40% recovery rate for loans already in default, rather than the 12% rate that Snowling uses, the pledge fund shortfall that so worries him simply disappears. More numbers on 2004-1:

The story is basically the same, by the way, on all the other trusts that has Snowling so worried. Plug in a 60% recovery rate, and it should be even more clear that the TERI pledge fund is more than sufficient.

So theres simply no problem here. As if to underscore that, Snowling himself admits that even under his own wacky numbers, the trusts in aggregate figure to generate positive cash of $20 million or so over their lives. Given that the pledge fund is sized to simply cover total net losses, this would imply that, overall, the credit quality of Marblehead-facilitated loans is actually better than expected using Snowlings own numbers, and not worse, as he maintains.

Put it all together, and I dont buy Snowlings concerns. The recovery assumptions hes making are way out of line with historical experienceand even then, the results that would occur arent as bad as he implies. I believe smart investors will see the stocks weakness for what it is: an opportunity to add at attractive prices.

|

http://seekingalpha.com/article/55549-fbr-s-latest-first-marblehead-downgrade-makes-no-sense?source=yahoo |

|

|

| Krypton |

Checked out the intrinsic strength of Citibank (C), and found something weird.

The intrinsic strength is -86.86

This is the first negative result I've had to look at. Well, why was negative?

Well, calculating the Free Cash Flow/Operating Cash Flow ratio gives me a very high negative.

Free cash flow is the cash left over from income AFTER the company has spent the money on capital expenditures. Citigroup's operating cash flow is a VERY LOW $13 million. Capital expenditures are $4.035 BILLION!! What!?!? That's a huge negative cash flow. The ratio comes out at -309.38 which throws off the intrinsic strength result completely.

The hallmark of a great company is one that has positive free cash flow. Citigroup has a huge negative cash flow, which while expected to be only temporary, prevent me from buying Citigroup even when the price, earnings, and dividends are cheap. Their cash flow statement is very alarming, with this negative cash flow that is HUGE, in the billions of dollars. They've cut their workforce by 10%, they are neck deep in CDO debt.

Now I can see why the stock has dropped this year; the CEO left and they just are suckin right now. I do think they will eventually get past it, but I would not buy at this point until they improved on their cash flows and other fundamentals. |

|

|

| Krypton |

| quote: | KFSF

* Name: Krypto Fundamental Strength Fund

* Net Asset Value (NAV): $11.26

* Compliant: Yes

* This past week

+ Return: 0.10%

+ Did you beat the:

o S&P 500 (return of -0.40%): YES

o NASDAQ (return of -0.65%): YES

o Dow Jones (return of -0.63%): YES

* Trailing 30 days

+ Return: 2.76%

+ Did you beat the:

o S&P 500 (return of 0.64%): YES

o NASDAQ (return of 0.43%): YES

o Dow Jones (return of 0.58%): YES |

This portfolio simply invests in stocks with fundamental strengths of 70 or higher.

Thesis: Companies whose fundamentals outperform in 3 categories; company vs. industry, company vs. market, and industry vs. market; will outperform the benchmark industry and market for that stock.

I think it's working....:D |

|

|

| Krypton |

I've been watching FMD like a hawk...

Check out the 1 week price chart....

http://ichart.finance.yahoo.com/w?s=FMD

It would appear that $15 is the level of support investors seem to not want to go below. This is the time I would buy FMD. So I am putting my real money where my mouth and I'm going to buy $200 of FMD. Wish me luck, though I won't need it~~!!!;)

EDIT:: So I put through an order for 11 shares of FMD at the market price of $15.15 .... I will not be using a stop loss .... I plan to hold for more than 1 year, buying more shares along the way.

I am going to follow my 'intrinsic strength financial model' to letter, and I very confident in my first choice of FMD, which my model found to be the most underpriced of the highly rated companies I have developed into my watchlist.

EDIT 2:: DAMMIT, my broker, ZECCO, has my account as a margin which requires $2000 minimum deposit. I was just on the phone with the broker asking why my FMD trade was REJECTED!! They told me I'm on margin, then I asked, "If I didn't have $2000 to open a margin account, why in the world am I in a margin account!? I know I didn't sign up for one...."

Well now, I have to send in a letter asking to switch my account. There goes the perfect buying opportunity I thought I had with FMD just touching what I think is a support level of $15. That ing letter isn't going to get there by Friday dammit!! I want to buy FMD right NOW!!!!! |

|

|

| Shakka |

| quote: | Originally posted by Krypton

I've been watching FMD like a hawk...

Check out the 1 week price chart....

http://ichart.finance.yahoo.com/w?s=FMD

It would appear that $15 is the level of support investors seem to not want to go below. This is the time I would buy FMD. So I am putting my real money where my mouth and I'm going to buy $200 of FMD. Wish me luck, though I won't need it~~!!!;)

EDIT:: So I put through an order for 11 shares of FMD at the market price of $15.15 .... I will not be using a stop loss .... I plan to hold for more than 1 year, buying more shares along the way.

I am going to follow my 'intrinsic strength financial model' to letter, and I very confident in my first choice of FMD, which my model found to be the most underpriced of the highly rated companies I have developed into my watchlist.

EDIT 2:: DAMMIT, my broker, ZECCO, has my account as a margin which requires $2000 minimum deposit. I was just on the phone with the broker asking why my FMD trade was REJECTED!! They told me I'm on margin, then I asked, "If I didn't have $2000 to open a margin account, why in the world am I in a margin account!? I know I didn't sign up for one...."

Well now, I have to send in a letter asking to switch my account. There goes the perfect buying opportunity I thought I had with FMD just touching what I think is a support level of $15. That ing letter isn't going to get there by Friday dammit!! I want to buy FMD right NOW!!!!! |

Consider yourself lucky. It's a POS. |

|

|

| Capitalizt |

I think he means piece of *** ;)

And I highly recommend you go with Scottrade for your broker...great website interface, flat $7 trades, extremely reliable, very good customer service, and local branches in every state. You can open an account online and hand your local branch a check tomorrow to start trading right away. :)

Scotrade.com |

|

|

| Krypton |

| quote: | Originally posted by Capitalizt

I think he means piece of *** ;)

And I highly recommend you go with Scottrade for your broker...great website interface, flat $7 trades, extremely reliable, very good customer service, and local branches in every state. You can open an account online and hand your local branch a check tomorrow to start trading right away. :)

Scotrade.com |

Eh, I already have 3. Zecco is $0 trades, so I'm trying it out.

I'm going to prove you wrong SHakka... We'll see by the end of 2008... |

|

|

| Shakka |

| quote: | Originally posted by Krypton

I'm going to prove you wrong SHakka... We'll see by the end of 2008... |

I wouldn't be surprised. But hey--you can buy FMD even cheaper today! My short will be covered before the end of the year (maybe covered and re-shorted multiple times if I can get the borrow!). Good luck! |

|

|

|

|